4. Elementary Probability with Matrices#

This lecture uses matrix algebra to illustrate some basic ideas about probability theory.

After providing somewhat informal definitions of the underlying objects, we’ll use matrices and vectors to describe probability distributions.

Among concepts that we’ll be studying include

a joint probability distribution

marginal distributions associated with a given joint distribution

conditional probability distributions

statistical independence of two random variables

joint distributions associated with a prescribed set of marginal distributions

couplings

copulas

the probability distribution of a sum of two independent random variables

convolution of marginal distributions

parameters that define a probability distribution

sufficient statistics as data summaries

We’ll use a matrix to represent a bivariate probability distribution and a vector to represent a univariate probability distribution

In addition to what’s in Anaconda, this lecture will need the following libraries:

!pip install prettytable

Show code cell output

Requirement already satisfied: prettytable in /opt/conda/envs/quantecon/lib/python3.11/site-packages (3.9.0)

Requirement already satisfied: wcwidth in /opt/conda/envs/quantecon/lib/python3.11/site-packages (from prettytable) (0.2.5)

WARNING: Running pip as the 'root' user can result in broken permissions and conflicting behaviour with the system package manager. It is recommended to use a virtual environment instead: https://pip.pypa.io/warnings/venv

As usual, we’ll start with some imports

import numpy as np

import matplotlib.pyplot as plt

import prettytable as pt

from mpl_toolkits.mplot3d import Axes3D

from matplotlib_inline.backend_inline import set_matplotlib_formats

set_matplotlib_formats('retina')

4.1. Sketch of Basic Concepts#

We’ll briefly define what we mean by a probability space, a probability measure, and a random variable.

For most of this lecture, we sweep these objects into the background, but they are there underlying the other objects that we’ll mainly focus on.

Let \(\Omega\) be a set of possible underlying outcomes and let \(\omega \in \Omega\) be a particular underlying outcomes.

Let \(\mathcal{G} \subset \Omega\) be a subset of \(\Omega\).

Let \(\mathcal{F}\) be a collection of such subsets \(\mathcal{G} \subset \Omega\).

The pair \(\Omega,\mathcal{F}\) forms our probability space on which we want to put a probability measure.

A probability measure \(\mu\) maps a set of possible underlying outcomes \(\mathcal{G} \in \mathcal{F}\) into a scalar number between \(0\) and \(1\)

this is the “probability” that \(X\) belongs to \(A\), denoted by \( \textrm{Prob}\{X\in A\}\).

A random variable \(X(\omega)\) is a function of the underlying outcome \(\omega \in \Omega\).

The random variable \(X(\omega)\) has a probability distribution that is induced by the underlying probability measure \(\mu\) and the function \(X(\omega)\):

where \({\mathcal G}\) is the subset of \(\Omega\) for which \(X(\omega) \in A\).

We call this the induced probability distribution of random variable \(X\).

4.2. What Does Probability Mean?#

Before diving in, we’ll say a few words about what probability theory means and how it connects to statistics.

We also touch on these topics in the quantecon lectures https://python.quantecon.org/prob_meaning.html and https://python.quantecon.org/navy_captain.html.

For much of this lecture we’ll be discussing fixed “population” probabilities.

These are purely mathematical objects.

To appreciate how statisticians connect probabilities to data, the key is to understand the following concepts:

A single draw from a probability distribution

Repeated independently and identically distributed (i.i.d.) draws of “samples” or “realizations” from the same probability distribution

A statistic defined as a function of a sequence of samples

An empirical distribution or histogram (a binned empirical distribution) that records observed relative frequencies

The idea that a population probability distribution is what we anticipate relative frequencies will be in a long sequence of i.i.d. draws. Here the following mathematical machinery makes precise what is meant by anticipated relative frequencies

Law of Large Numbers (LLN)

Central Limit Theorem (CLT)

Scalar example

Consider the following discrete distribution

Draw a sample \(x_0, x_1, \dots , x_{N-1}\), \(N\) draws of \(X\) from \(\{f_i\}^I_{i=1}\).

What do the “identical” and “independent” mean in IID or iid (“identically and independently distributed)?

“identical” means that each draw is from the same distribution.

“independent” means that the joint distribution equal tthe product of marginal distributions, i.e.,

Consider the empirical distribution:

Key ideas that justify connecting probability theory with statistics are laws of large numbers and central limit theorems

LLN:

A Law of Large Numbers (LLN) states that \(\tilde {f_i} \to f_i \text{ as } N \to \infty\)

CLT:

A Central Limit Theorem (CLT) describes a rate at which \(\tilde {f_i} \to f_i\)

Remarks

For “frequentist” statisticians, anticipated relative frequency is all that a probability distribution means.

But for a Bayesian it means something more or different.

4.3. Representing Probability Distributions#

A probability distribution \(\textrm{Prob} (X \in A)\) can be described by its cumulative distribution function (CDF)

Sometimes, but not always, a random variable can also be described by density function \(f(x)\) that is related to its CDF by

Here \(B\) is a set of possible \(X\)’s whose probability we want to compute.

When a probability density exists, a probability distribution can be characterized either by its CDF or by its density.

For a discrete-valued random variable

the number of possible values of \(X\) is finite or countably infinite

we replace a density with a probability mass function, a non-negative sequence that sums to one

we replace integration with summation in the formula like (4.1) that relates a CDF to a probability mass function

In this lecture, we mostly discuss discrete random variables.

Doing this enables us to confine our tool set basically to linear algebra.

Later we’ll briefly discuss how to approximate a continuous random variable with a discrete random variable.

4.4. Univariate Probability Distributions#

We’ll devote most of this lecture to discrete-valued random variables, but we’ll say a few things about continuous-valued random variables.

4.4.1. Discrete random variable#

Let \(X\) be a discrete random variable that takes possible values: \(i=0,1,\ldots,I-1 = \bar{X}\).

Here, we choose the maximum index \(I-1\) because of how this aligns nicely with Python’s index convention.

Define \(f_i \equiv \textrm{Prob}\{X=i\}\) and assemble the non-negative vector

for which \(f_{i} \in [0,1]\) for each \(i\) and \(\sum_{i=0}^{I-1}f_i=1\).

This vector defines a probability mass function.

The distribution (4.2) has parameters \(\{f_{i}\}_{i=0,1, \cdots ,I-2}\) since \(f_{I-1} = 1-\sum_{i=0}^{I-2}f_{i}\).

These parameters pin down the shape of the distribution.

(Sometimes \(I = \infty\).)

Such a “non-parametric” distribution has as many “parameters” as there are possible values of the random variable.

We often work with special distributions that are characterized by a small number parameters.

In these special parametric distributions,

where \(\theta \) is a vector of parameters that is of much smaller dimension than \(I\).

Remarks:

The concept of parameter is intimately related to the notion of sufficient statistic.

Sufficient statistics are nonlinear functions of a data set.

Sufficient statistics are designed to summarize all information about parameters that is contained in a data set.

They are important tools that AI uses to summarize a big data set

R. A. Fisher provided a rigorous definition of information – see https://en.wikipedia.org/wiki/Fisher_information

An example of a parametric probability distribution is a geometric distribution.

It is described by

Evidently, \(\sum_{i=0}^{\infty}f_i=1\).

Let \(\theta\) be a vector of parameters of the distribution described by \(f\), then

4.4.2. Continuous random variable#

Let \(X\) be a continous random variable that takes values \(X \in \tilde{X}\equiv[X_U,X_L]\) whose distributions have parameters \(\theta\).

where \(A\) is a subset of \(\tilde{X}\) and

4.5. Bivariate Probability Distributions#

We’ll now discuss a bivariate joint distribution.

To begin, we restrict ourselves to two discrete random variables.

Let \(X,Y\) be two discrete random variables that take values:

Then their joint distribution is described by a matrix

whose elements are

where

4.6. Marginal Probability Distributions#

The joint distribution induce marginal distributions

For example, let a joint distribution over \((X,Y)\) be

The implied marginal distributions are:

Digression: If two random variables \(X,Y\) are continuous and have joint density \(f(x,y)\), then marginal distributions can be computed by

4.7. Conditional Probability Distributions#

Conditional probabilities are defined according to

where \(A, B\) are two events.

For a pair of discrete random variables, we have the conditional distribution

where \(i=0, \ldots,I-1, \quad j=0,\ldots,J-1\).

Note that

Remark: The mathematics of conditional probability implies Bayes’ Law:

For the joint distribution (4.3)

4.8. Statistical Independence#

Random variables X and Y are statistically independent if

where

Conditional distributions are

4.9. Means and Variances#

The mean and variance of a discrete random variable \(X\) are

A continuous random variable having density \(f_{X}(x)\)) has mean and variance

4.10. Generating Random Numbers#

Suppose we have at our disposal a pseudo random number that draws a uniform random variable, i.e., one with probability distribution

How can we transform \(\tilde{X}\) to get a random variable \(X\) for which \(\textrm{Prob}\{X=i\}=f_i,\quad i=0,\ldots,I-1\), where \(f_i\) is an arbitary discrete probability distribution on \(i=0,1,\dots,I-1\)?

The key tool is the inverse of a cumulative distribution function (CDF).

Observe that the CDF of a distribution is monotone and non-decreasing, taking values between \(0\) and \(1\).

We can draw a sample of a random variable \(X\) with a known CDF as follows:

draw a random variable \(u\) from a uniform distribution on \([0,1]\)

pass the sample value of \(u\) into the “inverse” target CDF for \(X\)

\(X\) has the target CDF

Thus, knowing the “inverse” CDF of a distribution is enough to simulate from this distribution.

Note

The “inverse” CDF needs to exist for this method to work.

The inverse CDF is

Here we use infimum because a CDF is a non-decreasing and right-continuous function.

Thus, suppose that

\(U\) is a uniform random variable \(U\in[0,1]\)

We want to sample a random variable \(X\) whose CDF is \(F\).

It turns out that if we use draw uniform random numbers \(U\) and then compute \(X\) from

then \(X\) is a random variable with CDF \(F_X(x)=F(x)=\textrm{Prob}\{X\le x\}\).

We’ll verify this in the special case in which \(F\) is continuous and bijective so that its inverse function exists and can be denoted by \(F^{-1}\).

Note that

where the last equality occurs because \(U\) is distributed uniformly on \([0,1]\) while \(F(x)\) is a constant given \(x\) that also lies on \([0,1]\).

Let’s use numpy to compute some examples.

Example: A continuous geometric (exponential) distribution

Let \(X\) follow a geometric distribution, with parameter \(\lambda>0\).

Its density function is

Its CDF is

Let \(U\) follow a uniform distribution on \([0,1]\).

\(X\) is a random variable such that \(U=F(X)\).

The distribution \(X\) can be deduced from

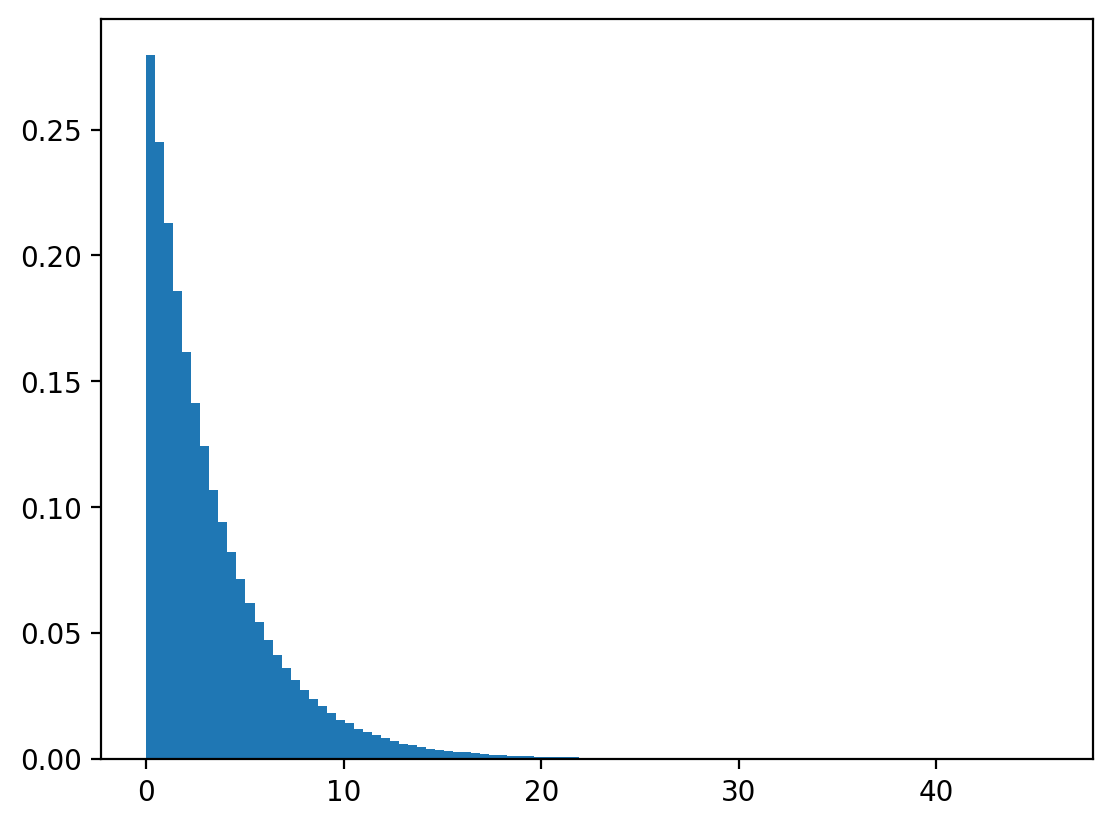

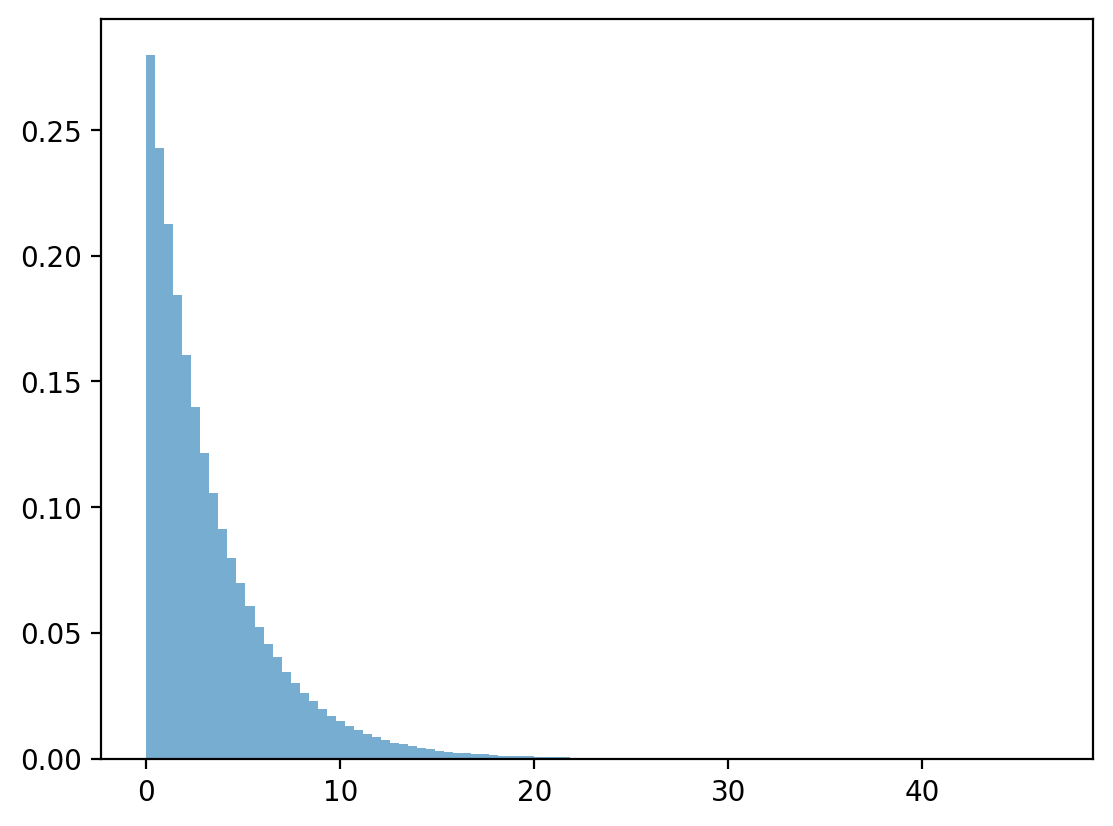

Let’s draw \(u\) from \(U[0,1]\) and calculate \(x=\frac{log(1-U)}{-\lambda}\).

We’ll check whether \(X\) seems to follow a continuous geometric (exponential) distribution.

Let’s check with numpy.

n, λ = 1_000_000, 0.3

# draw uniform numbers

u = np.random.rand(n)

# transform

x = -np.log(1-u)/λ

# draw geometric distributions

x_g = np.random.exponential(1 / λ, n)

# plot and compare

plt.hist(x, bins=100, density=True)

plt.show()

plt.hist(x_g, bins=100, density=True, alpha=0.6)

plt.show()

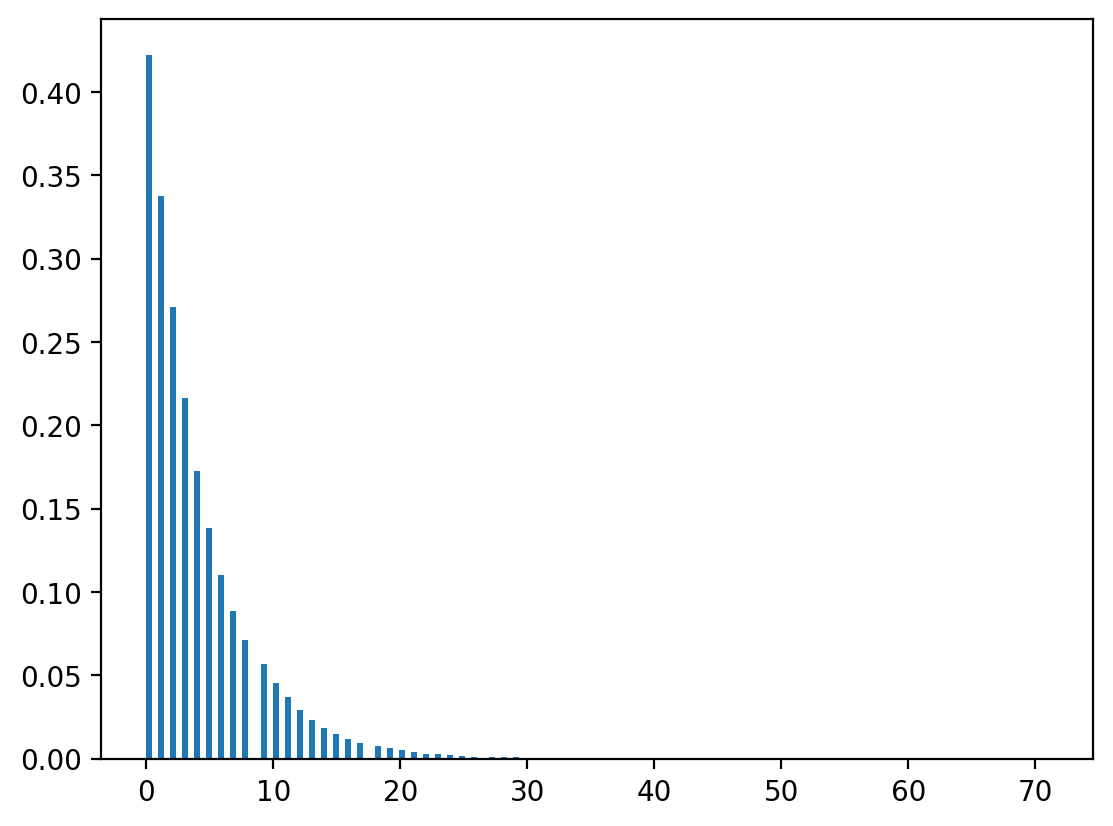

Geometric distribution

Let \(X\) distributed geometrically, that is

Its CDF is given by

Again, let \(\tilde{U}\) follow a uniform distribution and we want to find \(X\) such that \(F(X)=\tilde{U}\).

Let’s deduce the distribution of \(X\) from

However, \(\tilde{U}=F^{-1}(X)\) may not be an integer for any \(x\geq0\).

So let

where \(\lceil . \rceil\) is the ceiling function.

Thus \(x\) is the smallest integer such that the discrete geometric CDF is greater than or equal to \(\tilde{U}\).

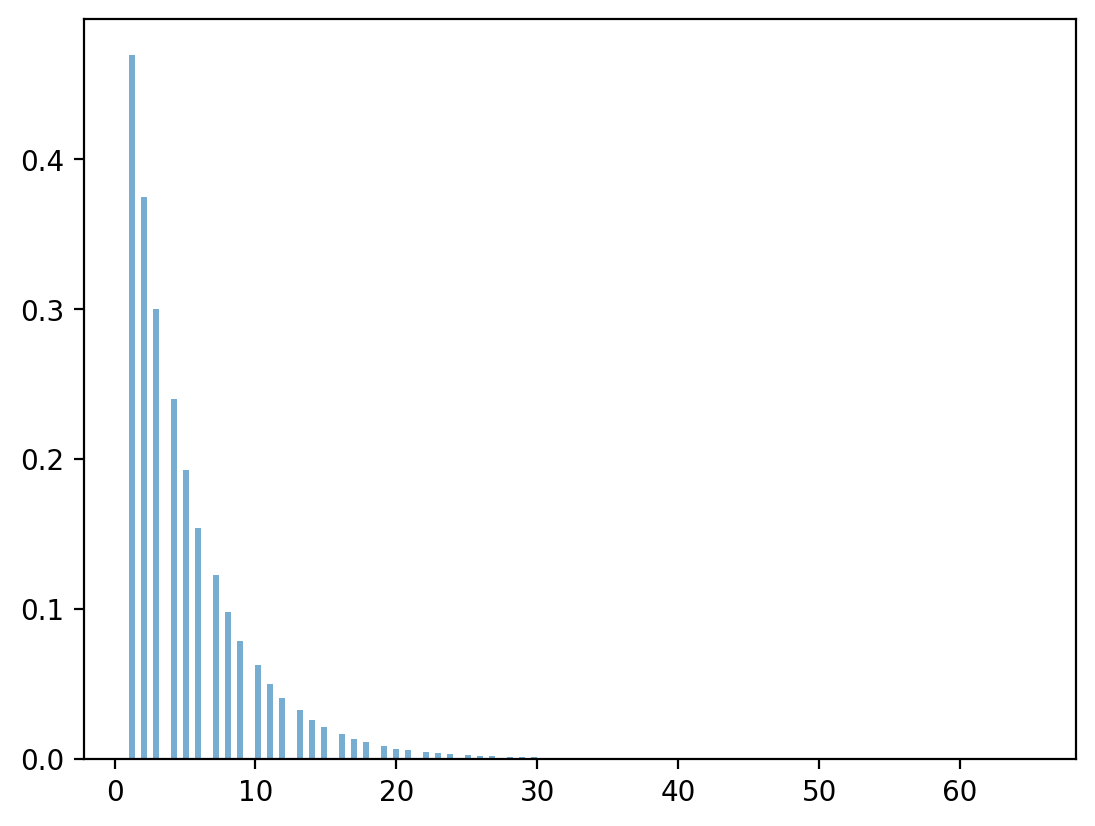

We can verify that \(x\) is indeed geometrically distributed by the following numpy program.

Note

The exponential distribution is the continuous analog of geometric distribution.

n, λ = 1_000_000, 0.8

# draw uniform numbers

u = np.random.rand(n)

# transform

x = np.ceil(np.log(1-u)/np.log(λ) - 1)

# draw geometric distributions

x_g = np.random.geometric(1-λ, n)

# plot and compare

plt.hist(x, bins=150, density=True)

plt.show()

np.random.geometric(1-λ, n).max()

55

np.log(0.4)/np.log(0.3)

0.7610560044063083

plt.hist(x_g, bins=150, density=True, alpha=0.6)

plt.show()

4.11. Some Discrete Probability Distributions#

Let’s write some Python code to compute means and variances of some univariate random variables.

We’ll use our code to

compute population means and variances from the probability distribution

generate a sample of \(N\) independently and identically distributed draws and compute sample means and variances

compare population and sample means and variances

4.12. Geometric distribution#

\(\implies\)

We draw observations from the distribution and compare the sample mean and variance with the theoretical results.

# specify parameters

p, n = 0.3, 1_000_000

# draw observations from the distribution

x = np.random.geometric(p, n)

# compute sample mean and variance

μ_hat = np.mean(x)

σ2_hat = np.var(x)

print("The sample mean is: ", μ_hat, "\nThe sample variance is: ", σ2_hat)

# compare with theoretical results

print("\nThe population mean is: ", 1/p)

print("The population variance is: ", (1-p)/(p**2))

The sample mean is: 3.328117

The sample variance is: 7.757662234311002

The population mean is: 3.3333333333333335

The population variance is: 7.777777777777778

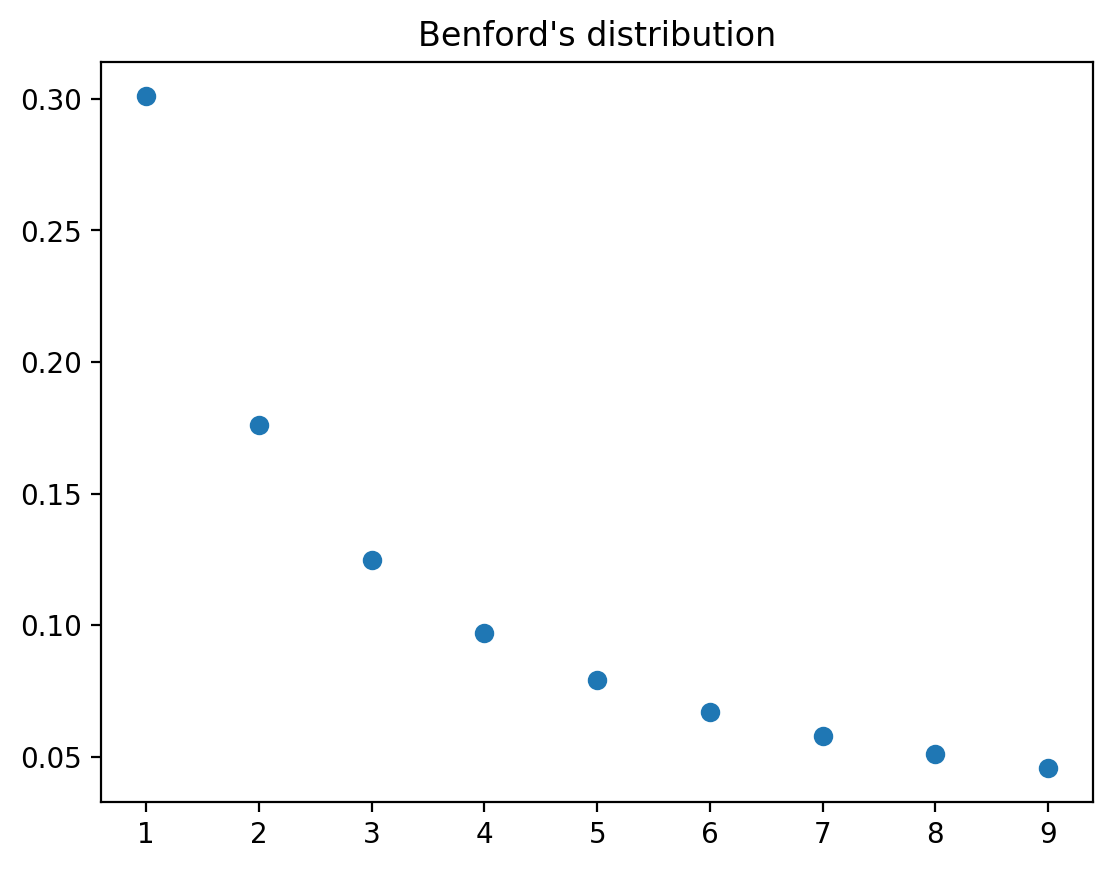

4.12.1. Newcomb–Benford distribution#

The Newcomb–Benford law fits many data sets, e.g., reports of incomes to tax authorities, in which the leading digit is more likely to be small than large.

See https://en.wikipedia.org/wiki/Benford’s_law

A Benford probability distribution is

where \(d\in\{1,2,\cdots,9\}\) can be thought of as a first digit in a sequence of digits.

This is a well defined discrete distribution since we can verify that probabilities are nonnegative and sum to \(1\).

The mean and variance of a Benford distribution are

We verify the above and compute the mean and variance using numpy.

Benford_pmf = np.array([np.log10(1+1/d) for d in range(1,10)])

k = np.array(range(1,10))

# mean

mean = np.sum(Benford_pmf * k)

# variance

var = np.sum([(k-mean)**2 * Benford_pmf])

# verify sum to 1

print(np.sum(Benford_pmf))

print(mean)

print(var)

0.9999999999999999

3.440236967123206

6.056512631375667

# plot distribution

plt.plot(range(1,10), Benford_pmf, 'o')

plt.title('Benford\'s distribution')

plt.show()

4.12.2. Pascal (negative binomial) distribution#

Consider a sequence of independent Bernoulli trials.

Let \(p\) be the probability of success.

Let \(X\) be a random variable that represents the number of failures before we get \(r\) success.

Its distribution is

Here, we choose from among \(k+r-1\) possible outcomes because the last draw is by definition a success.

We compute the mean and variance to be

# specify parameters

r, p, n = 10, 0.3, 1_000_000

# draw observations from the distribution

x = np.random.negative_binomial(r, p, n)

# compute sample mean and variance

μ_hat = np.mean(x)

σ2_hat = np.var(x)

print("The sample mean is: ", μ_hat, "\nThe sample variance is: ", σ2_hat)

print("\nThe population mean is: ", r*(1-p)/p)

print("The population variance is: ", r*(1-p)/p**2)

The sample mean is: 23.347525

The sample variance is: 77.84080337437506

The population mean is: 23.333333333333336

The population variance is: 77.77777777777779

4.13. Continuous Random Variables#

4.13.1. Univariate Gaussian distribution#

We write

to indicate the probability distribution

In the below example, we set \(\mu = 0, \sigma = 0.1\).

# specify parameters

μ, σ = 0, 0.1

# specify number of draws

n = 1_000_000

# draw observations from the distribution

x = np.random.normal(μ, σ, n)

# compute sample mean and variance

μ_hat = np.mean(x)

σ_hat = np.std(x)

print("The sample mean is: ", μ_hat)

print("The sample standard deviation is: ", σ_hat)

The sample mean is: -0.00011309665761054191

The sample standard deviation is: 0.0999698463189021

# compare

print(μ-μ_hat < 1e-3)

print(σ-σ_hat < 1e-3)

True

True

4.13.2. Uniform Distribution#

The population mean and variance are

# specify parameters

a, b = 10, 20

# specify number of draws

n = 1_000_000

# draw observations from the distribution

x = a + (b-a)*np.random.rand(n)

# compute sample mean and variance

μ_hat = np.mean(x)

σ2_hat = np.var(x)

print("The sample mean is: ", μ_hat, "\nThe sample variance is: ", σ2_hat)

print("\nThe population mean is: ", (a+b)/2)

print("The population variance is: ", (b-a)**2/12)

The sample mean is: 14.999655477794489

The sample variance is: 8.330771268334937

The population mean is: 15.0

The population variance is: 8.333333333333334

4.14. A Mixed Discrete-Continuous Distribution#

We’ll motivate this example with a little story.

Suppose that to apply for a job you take an interview and either pass or fail it.

You have \(5\%\) chance to pass an interview and you know your salary will uniformly distributed in the interval 300~400 a day only if you pass.

We can describe your daily salary as a discrete-continuous variable with the following probabilities:

Let’s start by generating a random sample and computing sample moments.

x = np.random.rand(1_000_000)

# x[x > 0.95] = 100*x[x > 0.95]+300

x[x > 0.95] = 100*np.random.rand(len(x[x > 0.95]))+300

x[x <= 0.95] = 0

μ_hat = np.mean(x)

σ2_hat = np.var(x)

print("The sample mean is: ", μ_hat, "\nThe sample variance is: ", σ2_hat)

The sample mean is: 17.346745634474946

The sample variance is: 5809.800328592666

The analytical mean and variance can be computed:

mean = 0.0005*0.5*(400**2 - 300**2)

var = 0.95*17.5**2+0.0005/3*((400-17.5)**3-(300-17.5)**3)

print("mean: ", mean)

print("variance: ", var)

mean: 17.5

variance: 5860.416666666666

4.15. Matrix Representation of Some Bivariate Distributions#

Let’s use matrices to represent a joint distribution, conditional distribution, marginal distribution, and the mean and variance of a bivariate random variable.

The table below illustrates a probability distribution for a bivariate random variable.

Marginal distributions are

Below we draw some samples confirm that the “sampling” distribution agrees well with the “population” distribution.

Sample results:

# specify parameters

xs = np.array([0, 1])

ys = np.array([10, 20])

f = np.array([[0.3, 0.2], [0.1, 0.4]])

f_cum = np.cumsum(f)

# draw random numbers

p = np.random.rand(1_000_000)

x = np.vstack([xs[1]*np.ones(p.shape), ys[1]*np.ones(p.shape)])

# map to the bivariate distribution

x[0, p < f_cum[2]] = xs[1]

x[1, p < f_cum[2]] = ys[0]

x[0, p < f_cum[1]] = xs[0]

x[1, p < f_cum[1]] = ys[1]

x[0, p < f_cum[0]] = xs[0]

x[1, p < f_cum[0]] = ys[0]

print(x)

[[ 1. 1. 0. ... 1. 1. 1.]

[10. 20. 20. ... 20. 10. 20.]]

Here, we use exactly the inverse CDF technique to generate sample from the joint distribution \(F\).

# marginal distribution

xp = np.sum(x[0, :] == xs[0])/1_000_000

yp = np.sum(x[1, :] == ys[0])/1_000_000

# print output

print("marginal distribution for x")

xmtb = pt.PrettyTable()

xmtb.field_names = ['x_value', 'x_prob']

xmtb.add_row([xs[0], xp])

xmtb.add_row([xs[1], 1-xp])

print(xmtb)

print("\nmarginal distribution for y")

ymtb = pt.PrettyTable()

ymtb.field_names = ['y_value', 'y_prob']

ymtb.add_row([ys[0], yp])

ymtb.add_row([ys[1], 1-yp])

print(ymtb)

marginal distribution for x

+---------+----------+

| x_value | x_prob |

+---------+----------+

| 0 | 0.499646 |

| 1 | 0.500354 |

+---------+----------+

marginal distribution for y

+---------+----------+

| y_value | y_prob |

+---------+----------+

| 10 | 0.399697 |

| 20 | 0.600303 |

+---------+----------+

# conditional distributions

xc1 = x[0, x[1, :] == ys[0]]

xc2 = x[0, x[1, :] == ys[1]]

yc1 = x[1, x[0, :] == xs[0]]

yc2 = x[1, x[0, :] == xs[1]]

xc1p = np.sum(xc1 == xs[0])/len(xc1)

xc2p = np.sum(xc2 == xs[0])/len(xc2)

yc1p = np.sum(yc1 == ys[0])/len(yc1)

yc2p = np.sum(yc2 == ys[0])/len(yc2)

# print output

print("conditional distribution for x")

xctb = pt.PrettyTable()

xctb.field_names = ['y_value', 'prob(x=0)', 'prob(x=1)']

xctb.add_row([ys[0], xc1p, 1-xc1p])

xctb.add_row([ys[1], xc2p, 1-xc2p])

print(xctb)

print("\nconditional distribution for y")

yctb = pt.PrettyTable()

yctb.field_names = ['x_value', 'prob(y=10)', 'prob(y=20)']

yctb.add_row([xs[0], yc1p, 1-yc1p])

yctb.add_row([xs[1], yc2p, 1-yc2p])

print(yctb)

conditional distribution for x

+---------+---------------------+---------------------+

| y_value | prob(x=0) | prob(x=1) |

+---------+---------------------+---------------------+

| 10 | 0.7502533168875423 | 0.24974668311245773 |

| 20 | 0.33278527676856523 | 0.6672147232314347 |

+---------+---------------------+---------------------+

conditional distribution for y

+---------+---------------------+--------------------+

| x_value | prob(y=10) | prob(y=20) |

+---------+---------------------+--------------------+

| 0 | 0.6001729224290798 | 0.3998270775709202 |

| 1 | 0.19950475063654932 | 0.8004952493634507 |

+---------+---------------------+--------------------+

Let’s calculate population marginal and conditional probabilities using matrix algebra.

\(\implies\)

(1) Marginal distribution:

(2) Conditional distribution:

These population objects closely resemble sample counterparts computed above.

Let’s wrap some of the functions we have used in a Python class for a general discrete bivariate joint distribution.

class discrete_bijoint:

def __init__(self, f, xs, ys):

'''initialization

-----------------

parameters:

f: the bivariate joint probability matrix

xs: values of x vector

ys: values of y vector

'''

self.f, self.xs, self.ys = f, xs, ys

def joint_tb(self):

'''print the joint distribution table'''

xs = self.xs

ys = self.ys

f = self.f

jtb = pt.PrettyTable()

jtb.field_names = ['x_value/y_value', *ys, 'marginal sum for x']

for i in range(len(xs)):

jtb.add_row([xs[i], *f[i, :], np.sum(f[i, :])])

jtb.add_row(['marginal_sum for y', *np.sum(f, 0), np.sum(f)])

print("\nThe joint probability distribution for x and y\n", jtb)

self.jtb = jtb

def draw(self, n):

'''draw random numbers

----------------------

parameters:

n: number of random numbers to draw

'''

xs = self.xs

ys = self.ys

f_cum = np.cumsum(self.f)

p = np.random.rand(n)

x = np.empty([2, p.shape[0]])

lf = len(f_cum)

lx = len(xs)-1

ly = len(ys)-1

for i in range(lf):

x[0, p < f_cum[lf-1-i]] = xs[lx]

x[1, p < f_cum[lf-1-i]] = ys[ly]

if ly == 0:

lx -= 1

ly = len(ys)-1

else:

ly -= 1

self.x = x

self.n = n

def marg_dist(self):

'''marginal distribution'''

x = self.x

xs = self.xs

ys = self.ys

n = self.n

xmp = [np.sum(x[0, :] == xs[i])/n for i in range(len(xs))]

ymp = [np.sum(x[1, :] == ys[i])/n for i in range(len(ys))]

# print output

xmtb = pt.PrettyTable()

ymtb = pt.PrettyTable()

xmtb.field_names = ['x_value', 'x_prob']

ymtb.field_names = ['y_value', 'y_prob']

for i in range(max(len(xs), len(ys))):

if i < len(xs):

xmtb.add_row([xs[i], xmp[i]])

if i < len(ys):

ymtb.add_row([ys[i], ymp[i]])

xmtb.add_row(['sum', np.sum(xmp)])

ymtb.add_row(['sum', np.sum(ymp)])

print("\nmarginal distribution for x\n", xmtb)

print("\nmarginal distribution for y\n", ymtb)

self.xmp = xmp

self.ymp = ymp

def cond_dist(self):

'''conditional distribution'''

x = self.x

xs = self.xs

ys = self.ys

n = self.n

xcp = np.empty([len(ys), len(xs)])

ycp = np.empty([len(xs), len(ys)])

for i in range(max(len(ys), len(xs))):

if i < len(ys):

xi = x[0, x[1, :] == ys[i]]

idx = xi.reshape(len(xi), 1) == xs.reshape(1, len(xs))

xcp[i, :] = np.sum(idx, 0)/len(xi)

if i < len(xs):

yi = x[1, x[0, :] == xs[i]]

idy = yi.reshape(len(yi), 1) == ys.reshape(1, len(ys))

ycp[i, :] = np.sum(idy, 0)/len(yi)

# print output

xctb = pt.PrettyTable()

yctb = pt.PrettyTable()

xctb.field_names = ['x_value', *xs, 'sum']

yctb.field_names = ['y_value', *ys, 'sum']

for i in range(max(len(xs), len(ys))):

if i < len(ys):

xctb.add_row([ys[i], *xcp[i], np.sum(xcp[i])])

if i < len(xs):

yctb.add_row([xs[i], *ycp[i], np.sum(ycp[i])])

print("\nconditional distribution for x\n", xctb)

print("\nconditional distribution for y\n", yctb)

self.xcp = xcp

self.xyp = ycp

Let’s apply our code to some examples.

Example 1

# joint

d = discrete_bijoint(f, xs, ys)

d.joint_tb()

The joint probability distribution for x and y

+--------------------+-----+--------------------+--------------------+

| x_value/y_value | 10 | 20 | marginal sum for x |

+--------------------+-----+--------------------+--------------------+

| 0 | 0.3 | 0.2 | 0.5 |

| 1 | 0.1 | 0.4 | 0.5 |

| marginal_sum for y | 0.4 | 0.6000000000000001 | 1.0 |

+--------------------+-----+--------------------+--------------------+

# sample marginal

d.draw(1_000_000)

d.marg_dist()

marginal distribution for x

+---------+----------+

| x_value | x_prob |

+---------+----------+

| 0 | 0.499354 |

| 1 | 0.500646 |

| sum | 1.0 |

+---------+----------+

marginal distribution for y

+---------+----------+

| y_value | y_prob |

+---------+----------+

| 10 | 0.399926 |

| 20 | 0.600074 |

| sum | 1.0 |

+---------+----------+

# sample conditional

d.cond_dist()

conditional distribution for x

+---------+---------------------+---------------------+-----+

| x_value | 0 | 1 | sum |

+---------+---------------------+---------------------+-----+

| 10 | 0.748493471292189 | 0.25150652870781093 | 1.0 |

| 20 | 0.33331222482560485 | 0.6666877751743951 | 1.0 |

+---------+---------------------+---------------------+-----+

conditional distribution for y

+---------+---------------------+--------------------+-----+

| y_value | 10 | 20 | sum |

+---------+---------------------+--------------------+-----+

| 0 | 0.5994585003824942 | 0.4005414996175058 | 1.0 |

| 1 | 0.20090842631320335 | 0.7990915736867966 | 1.0 |

+---------+---------------------+--------------------+-----+

Example 2

xs_new = np.array([10, 20, 30])

ys_new = np.array([1, 2])

f_new = np.array([[0.2, 0.1], [0.1, 0.3], [0.15, 0.15]])

d_new = discrete_bijoint(f_new, xs_new, ys_new)

d_new.joint_tb()

The joint probability distribution for x and y

+--------------------+---------------------+------+---------------------+

| x_value/y_value | 1 | 2 | marginal sum for x |

+--------------------+---------------------+------+---------------------+

| 10 | 0.2 | 0.1 | 0.30000000000000004 |

| 20 | 0.1 | 0.3 | 0.4 |

| 30 | 0.15 | 0.15 | 0.3 |

| marginal_sum for y | 0.45000000000000007 | 0.55 | 1.0 |

+--------------------+---------------------+------+---------------------+

d_new.draw(1_000_000)

d_new.marg_dist()

marginal distribution for x

+---------+----------+

| x_value | x_prob |

+---------+----------+

| 10 | 0.29986 |

| 20 | 0.399805 |

| 30 | 0.300335 |

| sum | 1.0 |

+---------+----------+

marginal distribution for y

+---------+---------+

| y_value | y_prob |

+---------+---------+

| 1 | 0.45002 |

| 2 | 0.54998 |

| sum | 1.0 |

+---------+---------+

d_new.cond_dist()

conditional distribution for x

+---------+--------------------+--------------------+--------------------+-----+

| x_value | 10 | 20 | 30 | sum |

+---------+--------------------+--------------------+--------------------+-----+

| 1 | 0.444689124927781 | 0.2221256833029643 | 0.3331851917692547 | 1.0 |

| 2 | 0.1813538674133605 | 0.5451907342085167 | 0.2734553983781228 | 1.0 |

+---------+--------------------+--------------------+--------------------+-----+

conditional distribution for y

+---------+---------------------+---------------------+-----+

| y_value | 1 | 2 | sum |

+---------+---------------------+---------------------+-----+

| 10 | 0.667374774894951 | 0.33262522510504905 | 1.0 |

| 20 | 0.2500243868886082 | 0.7499756131113918 | 1.0 |

| 30 | 0.49924251252767743 | 0.5007574874723226 | 1.0 |

+---------+---------------------+---------------------+-----+

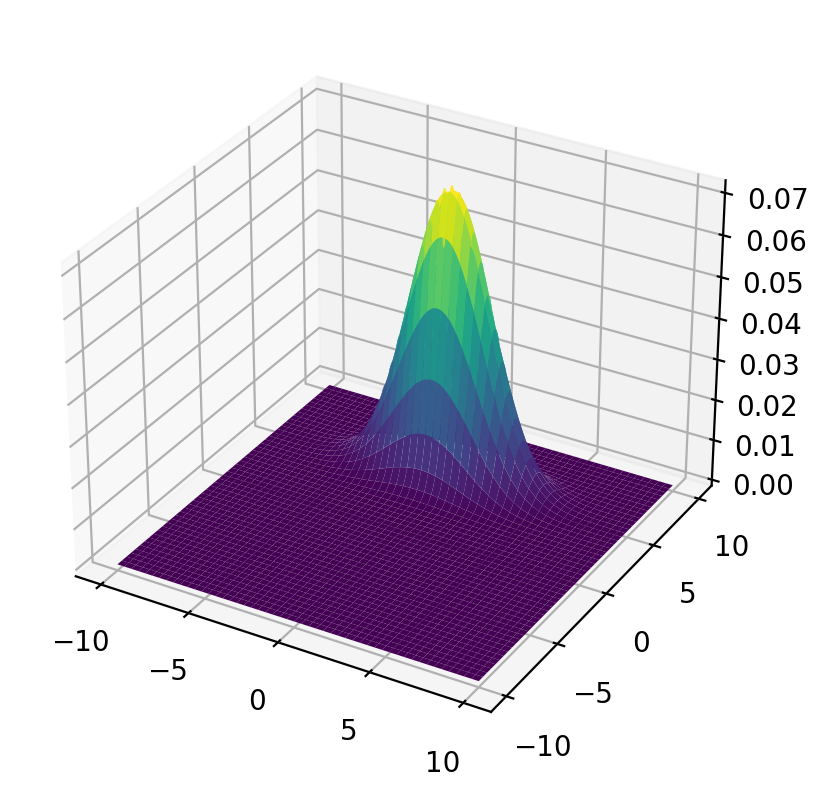

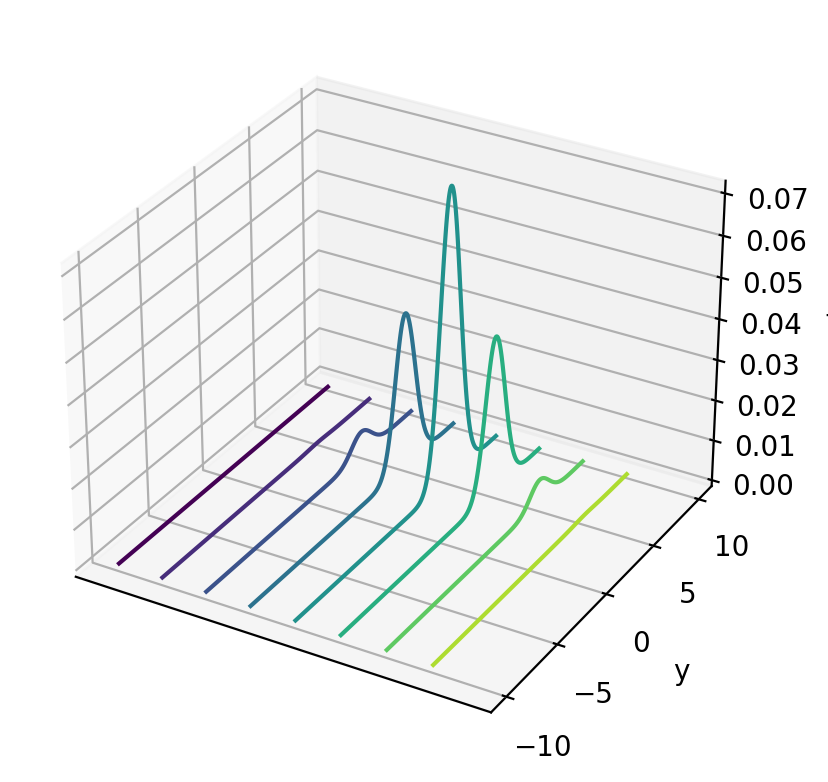

4.16. A Continuous Bivariate Random Vector#

A two-dimensional Gaussian distribution has joint density

We start with a bivariate normal distribution pinned down by

# define the joint probability density function

def func(x, y, μ1=0, μ2=5, σ1=np.sqrt(5), σ2=np.sqrt(1), ρ=.2/np.sqrt(5*1)):

A = (2 * np.pi * σ1 * σ2 * np.sqrt(1 - ρ**2))**(-1)

B = -1 / 2 / (1 - ρ**2)

C1 = (x - μ1)**2 / σ1**2

C2 = 2 * ρ * (x - μ1) * (y - μ2) / σ1 / σ2

C3 = (y - μ2)**2 / σ2**2

return A * np.exp(B * (C1 - C2 + C3))

μ1 = 0

μ2 = 5

σ1 = np.sqrt(5)

σ2 = np.sqrt(1)

ρ = .2 / np.sqrt(5 * 1)

x = np.linspace(-10, 10, 1_000)

y = np.linspace(-10, 10, 1_000)

x_mesh, y_mesh = np.meshgrid(x, y, indexing="ij")

Joint Distribution

Let’s plot the population joint density.

# %matplotlib notebook

fig = plt.figure()

ax = plt.axes(projection='3d')

surf = ax.plot_surface(x_mesh, y_mesh, func(x_mesh, y_mesh), cmap='viridis')

plt.show()

# %matplotlib notebook

fig = plt.figure()

ax = plt.axes(projection='3d')

curve = ax.contour(x_mesh, y_mesh, func(x_mesh, y_mesh), zdir='x')

plt.ylabel('y')

ax.set_zlabel('f')

ax.set_xticks([])

plt.show()

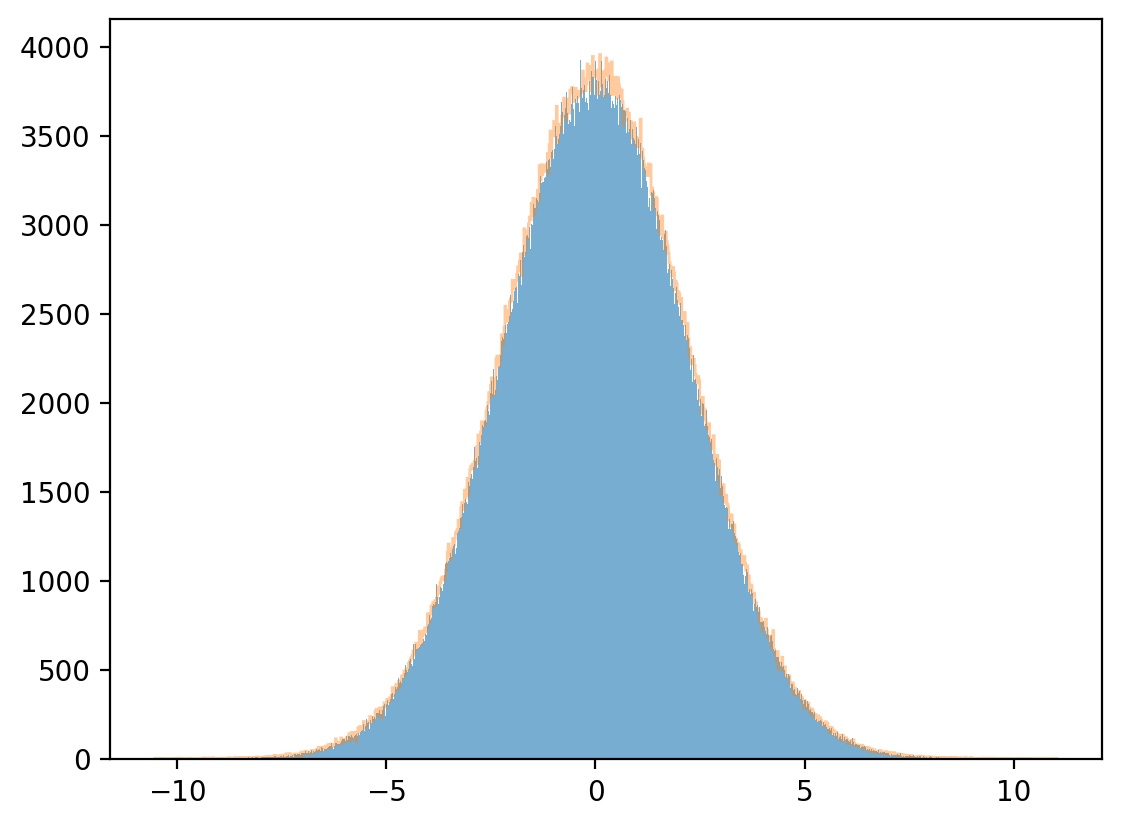

Next we can simulate from a built-in numpy function and calculate a sample marginal distribution from the sample mean and variance.

μ= np.array([0, 5])

σ= np.array([[5, .2], [.2, 1]])

n = 1_000_000

data = np.random.multivariate_normal(μ, σ, n)

x = data[:, 0]

y = data[:, 1]

Marginal distribution

plt.hist(x, bins=1_000, alpha=0.6)

μx_hat, σx_hat = np.mean(x), np.std(x)

print(μx_hat, σx_hat)

x_sim = np.random.normal(μx_hat, σx_hat, 1_000_000)

plt.hist(x_sim, bins=1_000, alpha=0.4, histtype="step")

plt.show()

0.0004958360623134676 2.2355510116371384

plt.hist(y, bins=1_000, density=True, alpha=0.6)

μy_hat, σy_hat = np.mean(y), np.std(y)

print(μy_hat, σy_hat)

y_sim = np.random.normal(μy_hat, σy_hat, 1_000_000)

plt.hist(y_sim, bins=1_000, density=True, alpha=0.4, histtype="step")

plt.show()

4.99953178052401 0.9994150311616088

Conditional distribution

The population conditional distribution is

Let’s approximate the joint density by discretizing and mapping the approximating joint density into a matrix.

We can compute the discretized marginal density by just using matrix algebra and noting that

Fix \(y=0\).

# discretized marginal density

x = np.linspace(-10, 10, 1_000_000)

z = func(x, y=0) / np.sum(func(x, y=0))

plt.plot(x, z)

plt.show()

The mean and variance are computed by

Let’s draw from a normal distribution with above mean and variance and check how accurate our approximation is.

# discretized mean

μx = np.dot(x, z)

# discretized standard deviation

σx = np.sqrt(np.dot((x - μx)**2, z))

# sample

zz = np.random.normal(μx, σx, 1_000_000)

plt.hist(zz, bins=300, density=True, alpha=0.3, range=[-10, 10])

plt.show()

Fix \(x=1\).

y = np.linspace(0, 10, 1_000_000)

z = func(x=1, y=y) / np.sum(func(x=1, y=y))

plt.plot(y,z)

plt.show()

# discretized mean and standard deviation

μy = np.dot(y,z)

σy = np.sqrt(np.dot((y - μy)**2, z))

# sample

zz = np.random.normal(μy,σy,1_000_000)

plt.hist(zz, bins=100, density=True, alpha=0.3)

plt.show()

We compare with the analytically computed parameters and note that they are close.

print(μx, σx)

print(μ1 + ρ * σ1 * (0 - μ2) / σ2, np.sqrt(σ1**2 * (1 - ρ**2)))

print(μy, σy)

print(μ2 + ρ * σ2 * (1 - μ1) / σ1, np.sqrt(σ2**2 * (1 - ρ**2)))

-0.9997518414498433 2.22658413316977

-1.0 2.227105745132009

5.039999456960768 0.9959851265795597

5.04 0.9959919678390986

4.17. Sum of Two Independently Distributed Random Variables#

Let \(X, Y\) be two independent discrete random variables that take values in \(\bar{X}, \bar{Y}\), respectively.

Define a new random variable \(Z=X+Y\).

Evidently, \(Z\) takes values from \(\bar{Z}\) defined as follows:

Independence of \(X\) and \( Y\) implies that

Thus, we have:

where \(f * g\) denotes the convolution of the \(f\) and \(g\) sequences.

Similarly, for two random variables \(X,Y\) with densities \(f_{X}, g_{Y}\), the density of \(Z=X+Y\) is

where \( f_{X}*g_{Y} \) denotes the convolution of the \(f_X\) and \(g_Y\) functions.

4.18. Transition Probability Matrix#

Consider the following joint probability distribution of two random variables.

Let \(X,Y\) be discrete random variables with joint distribution

where \(i = 0,\dots,I-1; j = 0,\dots,J-1\) and

An associated conditional distribution is

We can define a transition probability matrix

where

The first row is the probability of \(Y=j, j=0,1\) conditional on \(X=0\).

The second row is the probability of \(Y=j, j=0,1\) conditional on \(X=1\).

Note that

\(\sum_{j}\rho_{ij}= \frac{ \sum_{j}\rho_{ij}}{ \sum_{j}\rho_{ij}}=1\), so each row of \(\rho\) is a probability distribution (not so for each column.

4.19. Coupling#

Start with a joint distribution

where

From the joint distribution, we have shown above that we obtain unique marginal distributions.

Now we’ll try to go in a reverse direction.

We’ll find that from two marginal distributions, can we usually construct more than one joint distribution that verifies these marginals.

Each of these joint distributions is called a coupling of the two martingal distributions.

Let’s start with marginal distributions

Given two marginal distribution, \(\mu\) for \(X\) and \(\nu\) for \(Y\), a joint distribution \(f_{ij}\) is said to be a coupling of \(\mu\) and \(\nu\).

Example:

Consider the following bivariate example.

We construct two couplings.

The first coupling if our two marginal distributions is the joint distribution

To verify that it is a coupling, we check that

A second coupling of our two marginal distributions is the joint distribution

The verify that this is a coupling, note that

Thus, our two proposed joint distributions have the same marginal distributions.

But the joint distributions differ.

Thus, multiple joint distributions \([f_{ij}]\) can have the same marginals.

Remark:

Couplings are important in optimal transport problems and in Markov processes.

4.20. Copula Functions#

Suppose that \(X_1, X_2, \dots, X_n\) are \(N\) random variables and that

their marginal distributions are \(F_1(x_1), F_2(x_2),\dots, F_N(x_N)\), and

their joint distribution is \(H(x_1,x_2,\dots,x_N)\)

Then there exists a copula function \(C(\cdot)\) that verifies

We can obtain

In a reverse direction of logic, given univariate marginal distributions \(F_1(x_1), F_2(x_2),\dots,F_N(x_N)\) and a copula function \(C(\cdot)\), the function \(H(x_1,x_2,\dots,x_N) = C(F_1(x_1), F_2(x_2),\dots,F_N(x_N))\) is a coupling of \(F_1(x_1), F_2(x_2),\dots,F_N(x_N)\).

Thus, for given marginal distributions, we can use a copula function to determine a joint distribution when the associated univariate random variables are not independent.

Copula functions are often used to characterize dependence of random variables.

Discrete marginal distribution

As mentioned above, for two given marginal distributions there can be more than one coupling.

For example, consider two random variables \(X, Y\) with distributions

For these two random variables there can be more than one coupling.

Let’s first generate X and Y.

# define parameters

mu = np.array([0.6, 0.4])

nu = np.array([0.3, 0.7])

# number of draws

draws = 1_000_000

# generate draws from uniform distribution

p = np.random.rand(draws)

# generate draws of X and Y via uniform distribution

x = np.ones(draws)

y = np.ones(draws)

x[p <= mu[0]] = 0

x[p > mu[0]] = 1

y[p <= nu[0]] = 0

y[p > nu[0]] = 1

# calculate parameters from draws

q_hat = sum(x[x == 1])/draws

r_hat = sum(y[y == 1])/draws

# print output

print("distribution for x")

xmtb = pt.PrettyTable()

xmtb.field_names = ['x_value', 'x_prob']

xmtb.add_row([0, 1-q_hat])

xmtb.add_row([1, q_hat])

print(xmtb)

print("distribution for y")

ymtb = pt.PrettyTable()

ymtb.field_names = ['y_value', 'y_prob']

ymtb.add_row([0, 1-r_hat])

ymtb.add_row([1, r_hat])

print(ymtb)

distribution for x

+---------+--------------------+

| x_value | x_prob |

+---------+--------------------+

| 0 | 0.6000639999999999 |

| 1 | 0.399936 |

+---------+--------------------+

distribution for y

+---------+----------+

| y_value | y_prob |

+---------+----------+

| 0 | 0.299975 |

| 1 | 0.700025 |

+---------+----------+

Let’s now take our two marginal distributions, one for \(X\), the other for \(Y\), and construct two distinct couplings.

For the first joint distribution:

where

Let’s use Python to construct this joint distribution and then verify that its marginal distributions are what we want.

# define parameters

f1 = np.array([[0.18, 0.42], [0.12, 0.28]])

f1_cum = np.cumsum(f1)

# number of draws

draws1 = 1_000_000

# generate draws from uniform distribution

p = np.random.rand(draws1)

# generate draws of first copuling via uniform distribution

c1 = np.vstack([np.ones(draws1), np.ones(draws1)])

# X=0, Y=0

c1[0, p <= f1_cum[0]] = 0

c1[1, p <= f1_cum[0]] = 0

# X=0, Y=1

c1[0, (p > f1_cum[0])*(p <= f1_cum[1])] = 0

c1[1, (p > f1_cum[0])*(p <= f1_cum[1])] = 1

# X=1, Y=0

c1[0, (p > f1_cum[1])*(p <= f1_cum[2])] = 1

c1[1, (p > f1_cum[1])*(p <= f1_cum[2])] = 0

# X=1, Y=1

c1[0, (p > f1_cum[2])*(p <= f1_cum[3])] = 1

c1[1, (p > f1_cum[2])*(p <= f1_cum[3])] = 1

# calculate parameters from draws

f1_00 = sum((c1[0, :] == 0)*(c1[1, :] == 0))/draws1

f1_01 = sum((c1[0, :] == 0)*(c1[1, :] == 1))/draws1

f1_10 = sum((c1[0, :] == 1)*(c1[1, :] == 0))/draws1

f1_11 = sum((c1[0, :] == 1)*(c1[1, :] == 1))/draws1

# print output of first joint distribution

print("first joint distribution for c1")

c1_mtb = pt.PrettyTable()

c1_mtb.field_names = ['c1_x_value', 'c1_y_value', 'c1_prob']

c1_mtb.add_row([0, 0, f1_00])

c1_mtb.add_row([0, 1, f1_01])

c1_mtb.add_row([1, 0, f1_10])

c1_mtb.add_row([1, 1, f1_11])

print(c1_mtb)

first joint distribution for c1

+------------+------------+----------+

| c1_x_value | c1_y_value | c1_prob |

+------------+------------+----------+

| 0 | 0 | 0.1804 |

| 0 | 1 | 0.420325 |

| 1 | 0 | 0.119486 |

| 1 | 1 | 0.279789 |

+------------+------------+----------+

# calculate parameters from draws

c1_q_hat = sum(c1[0, :] == 1)/draws1

c1_r_hat = sum(c1[1, :] == 1)/draws1

# print output

print("marginal distribution for x")

c1_x_mtb = pt.PrettyTable()

c1_x_mtb.field_names = ['c1_x_value', 'c1_x_prob']

c1_x_mtb.add_row([0, 1-c1_q_hat])

c1_x_mtb.add_row([1, c1_q_hat])

print(c1_x_mtb)

print("marginal distribution for y")

c1_ymtb = pt.PrettyTable()

c1_ymtb.field_names = ['c1_y_value', 'c1_y_prob']

c1_ymtb.add_row([0, 1-c1_r_hat])

c1_ymtb.add_row([1, c1_r_hat])

print(c1_ymtb)

marginal distribution for x

+------------+-----------+

| c1_x_value | c1_x_prob |

+------------+-----------+

| 0 | 0.600725 |

| 1 | 0.399275 |

+------------+-----------+

marginal distribution for y

+------------+-----------+

| c1_y_value | c1_y_prob |

+------------+-----------+

| 0 | 0.299886 |

| 1 | 0.700114 |

+------------+-----------+

Now, let’s construct another joint distribution that is also a coupling of \(X\) and \(Y\)

# define parameters

f2 = np.array([[0.3, 0.3], [0, 0.4]])

f2_cum = np.cumsum(f2)

# number of draws

draws2 = 1_000_000

# generate draws from uniform distribution

p = np.random.rand(draws2)

# generate draws of first coupling via uniform distribution

c2 = np.vstack([np.ones(draws2), np.ones(draws2)])

# X=0, Y=0

c2[0, p <= f2_cum[0]] = 0

c2[1, p <= f2_cum[0]] = 0

# X=0, Y=1

c2[0, (p > f2_cum[0])*(p <= f2_cum[1])] = 0

c2[1, (p > f2_cum[0])*(p <= f2_cum[1])] = 1

# X=1, Y=0

c2[0, (p > f2_cum[1])*(p <= f2_cum[2])] = 1

c2[1, (p > f2_cum[1])*(p <= f2_cum[2])] = 0

# X=1, Y=1

c2[0, (p > f2_cum[2])*(p <= f2_cum[3])] = 1

c2[1, (p > f2_cum[2])*(p <= f2_cum[3])] = 1

# calculate parameters from draws

f2_00 = sum((c2[0, :] == 0)*(c2[1, :] == 0))/draws2

f2_01 = sum((c2[0, :] == 0)*(c2[1, :] == 1))/draws2

f2_10 = sum((c2[0, :] == 1)*(c2[1, :] == 0))/draws2

f2_11 = sum((c2[0, :] == 1)*(c2[1, :] == 1))/draws2

# print output of second joint distribution

print("first joint distribution for c2")

c2_mtb = pt.PrettyTable()

c2_mtb.field_names = ['c2_x_value', 'c2_y_value', 'c2_prob']

c2_mtb.add_row([0, 0, f2_00])

c2_mtb.add_row([0, 1, f2_01])

c2_mtb.add_row([1, 0, f2_10])

c2_mtb.add_row([1, 1, f2_11])

print(c2_mtb)

first joint distribution for c2

+------------+------------+----------+

| c2_x_value | c2_y_value | c2_prob |

+------------+------------+----------+

| 0 | 0 | 0.29999 |

| 0 | 1 | 0.300061 |

| 1 | 0 | 0.0 |

| 1 | 1 | 0.399949 |

+------------+------------+----------+

# calculate parameters from draws

c2_q_hat = sum(c2[0, :] == 1)/draws2

c2_r_hat = sum(c2[1, :] == 1)/draws2

# print output

print("marginal distribution for x")

c2_x_mtb = pt.PrettyTable()

c2_x_mtb.field_names = ['c2_x_value', 'c2_x_prob']

c2_x_mtb.add_row([0, 1-c2_q_hat])

c2_x_mtb.add_row([1, c2_q_hat])

print(c2_x_mtb)

print("marginal distribution for y")

c2_ymtb = pt.PrettyTable()

c2_ymtb.field_names = ['c2_y_value', 'c2_y_prob']

c2_ymtb.add_row([0, 1-c2_r_hat])

c2_ymtb.add_row([1, c2_r_hat])

print(c2_ymtb)

marginal distribution for x

+------------+-----------+

| c2_x_value | c2_x_prob |

+------------+-----------+

| 0 | 0.600051 |

| 1 | 0.399949 |

+------------+-----------+

marginal distribution for y

+------------+-----------+

| c2_y_value | c2_y_prob |

+------------+-----------+

| 0 | 0.29999 |

| 1 | 0.70001 |

+------------+-----------+

We have verified that both joint distributions, \(c_1\) and \(c_2\), have identical marginal distributions of \(X\) and \(Y\), respectively.

So they are both couplings of \(X\) and \(Y\).

4.21. Time Series#

Suppose that there are two time periods.

\(t=0\) “today”

\(t=1\) “tomorrow”

Let \(X(0)\) be a random variable to be realized at \(t=0\), \(X(1)\) be a random variable to be realized at \(t=1\).

Suppose that

\(f_{ij} \) is a joint distribution over \([X(0), X(1)]\).

A conditional distribution is

Remark:

This is a key formula for a theory of optimally predicting a time series.